Fintech has made it easier for ordinary retail investors to discover new opportunities through innovation in crowdsourcing. Investors can participate directly as shareholders of private enterprises via equity crowd funding (ECF) or become lenders via peer-to-peer financing (P2P).

Conversely, these enterprises gain access to new capital pools beyond their immediate network of families and friends. Or they get to tap into alternative funding sources after exhausting the credit lines in their banking relationships.

Initial Exchange Offering (IEO) opens another avenue for them. Theoretically, digital assets are borderless and enable free movement of capital. This means that IEO can potentially attract global capital inflows for local enterprises, which is an advantage vis-à-vis ECF and P2P.

A Boon for Local Tech Entrepreneurs?

We know that the financing gap for micro-, small- and medium enterprises (MSME) has always been a perennial problem. This is a key growth engine for the economy but lack funding options. Based on estimates by the Securities Commission (SC), the MSME segment contributes around 60% of our country’s gross domestic product (GDP) but face a financing gap of RM90 billion.

[1] Funding from conventional equity and bond markets mainly cater to listed companies, even though they contribute to only an estimated 15% of GDP.

In the technology sector, which is typically loss-making in the early stages, the problem is more acute. It has to rely on a limited base of angel investors, government grants, and onshore venture capital (VC) funds, many of which are also government-linked.

It doesn’t help either that the local VC landscape is less robust compared to our neighbours like Singapore and Indonesia – with fewer active firms, smaller fund sizes, and lower risk appetite.

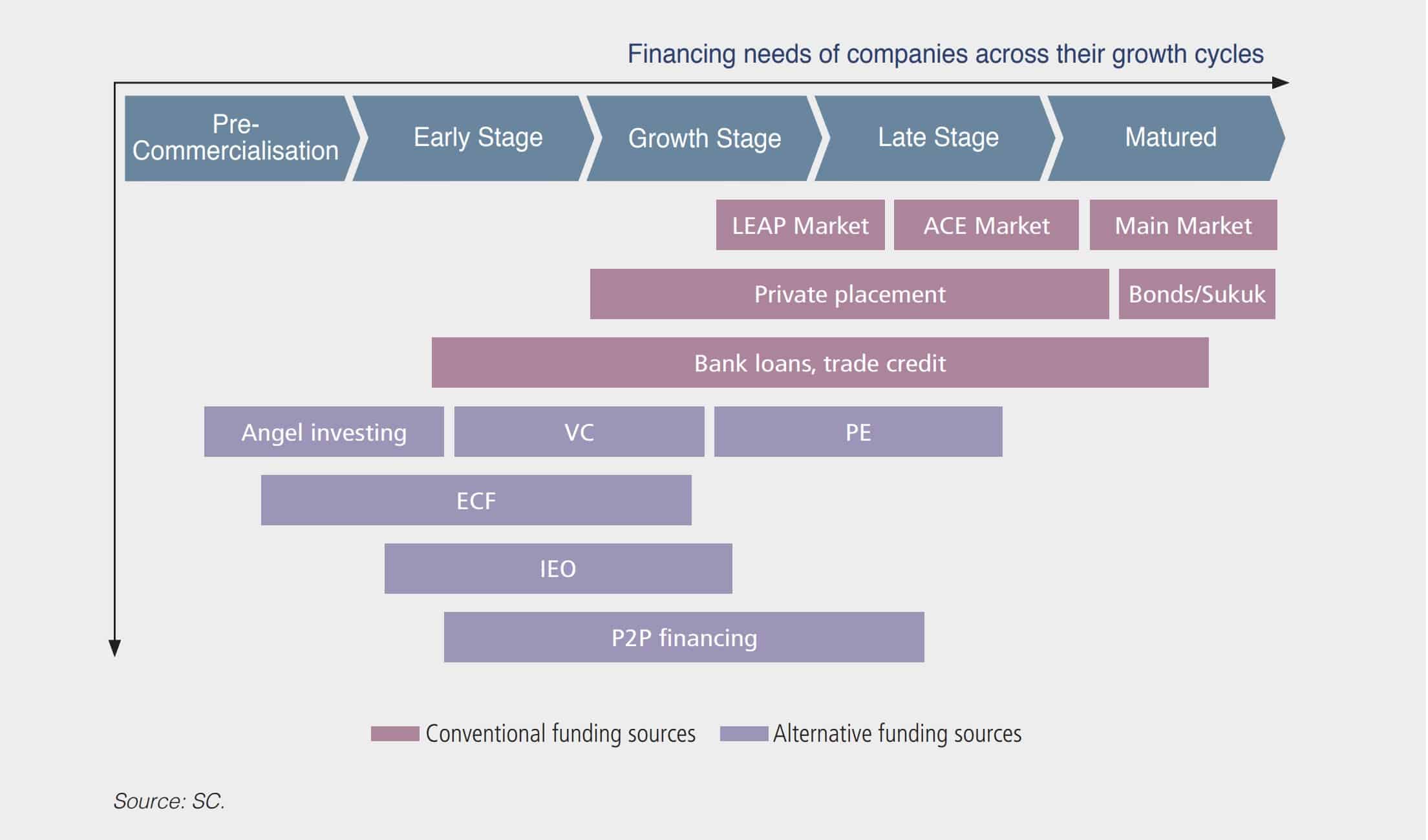

This is where IEOs come in to fill this gap, as an alternative tool for enterprises to form capital across their spectrum of growth (see diagram).

IEOs specifically cater to enterprises with projects that “provide an innovative solution or a meaningful digital value proposition for Malaysia”.[2] This is wide enough to include anything that “addresses an existing market need or problem; or improves the efficiency of an existing process or service”.

By allowing IEOs to raise up to a maximum of RM100 million, this could carry start-ups and early-stagers through to the Series rounds. In fact, this amount is even higher than what late-stagers averagely raise at public listings on the junior boards of Bursa Malaysia like ACE and LEAP!

Source: Securities Commission Malaysia

Is it Difficult to Become an Issuer?

While there are regulatory requirements to ensure the integrity of the offering, the funds are kept in trusted hands, and the people running the show are fit and proper – overall, the entry barrier is kept low. If you are planning to issue tokens for your business, you can approach the IEO operator who will qualify your investment thesis and make the decision to approve or reject it. It does not have to go through SC for approval.

What you do need is to prepare a whitepaper for submission to the IEO operator and SC. Although this is not subject to stringent Prospectus Guidelines, the requisite coverage of contents is extensive. Put bluntly, this is not going to be any run-of-the-mill whitepaper of an Initial Coin Offering (ICO) project that you just pull from the web.

It has to include, among other things, the audited financial statements of the issuer, distribution policy of the digital tokens, their accounting and valuation treatments including “all reasonable presumptions adopted in such calculation”, and the scheduled timeline for drawdown and utilisation of proceeds.[3] And should there be any material changes or omission to the whitepaper, a supplement is required for submission anew.

The issuer should also note that an IEO is an ‘all-or-nothing’ raise. Essentially what this means is that the issuance must be fully subscribed. If it is under-subscribed, the issuer is not allowed to keep the monies raised unless the target amount is achieved, and the IEO operator must refund back to investors. If it is over-subscribed, the issuer is not allowed to keep any amount exceeding the target amount raised.

Does This Replace Venture Capital?

No, it doesn’t. The intent is to diversify funding sources as shown in the diagram above. But there are other factors at play.

To the cash-hungry entrepreneur, the IEO option generally provides lower cost of funds with lower cost of issuance (though this is debatable). Their investors are less demanding than banks when it comes to assessing the credit risk profile of the enterprise.

More importantly, digital tokens are not considered shares (as mentioned in Part 1) and are thus non-dilutive to capital structure. The shareholding control and cap table will remain the same post-IEO.

On the other hand, VCs may prefer the conventional funding route for their investees because digital token issuance can complicate valuation during investment rounds and cause problems for eventual public listing. Why would VCs want to accept digital tokens, which might seem legally untested, instead of the usual tried-and-true convertible notes?

Furthermore, the VC contract includes detailed covenants and provisions which cannot be summarily replaced by the ‘smart contract’ used in digital tokens in an IEO relationship.

And while there are global ‘crypto VCs’ that do accept digital tokens, they face a hurdle in Malaysian IEOs because cryptocurrency is not allowed as a form of payment for investment. More on this in Part 3.

One thing to note is that IEOs cannot provide the kind of support that VCs do: To incubate, mentor, and accelerate the business. This is a major lesson from the ICO Boom-Bust during the 2016-19 period: While most people think of ICOs as scams or money grabs, the truth is, many projects were genuine without malicious intent, but their entrepreneurs didn’t know how to handle too much investors’ money and ended up failing. Cheap and easy capital can be both a blessing and a curse!

Simply said: IEOs can give what entrepreneurs want but not necessarily what they need. The IEO regulations ensure that there is accountability for the funds raised – but not the advisory to prevent these funds from being misused by management.

Why Are Other Sectors Also Eyeing This?

The ability to tokenise assets and businesses into units of investment, and distribute them through IEOs, has captured the imagination of other industries such as property, agriculture, and hospitality.

For lumpy or indivisible assets like real estate or property, tokenisation can carve them up conceptually into smaller affordable portions (commonly known as ‘fractionalisation’) with lower minimum investment for retail investors. For commoditised sectors like agriculture, the issuer can sell digital tokens that represent metric units of their production yield e.g., one token equals to one tonne of wheat.

It boils down to how you play with the economics: Hotels are intuitively tokenisable as they are made up of individual rooms which generate income. Investors can estimate how much a hotel room unit is worth based on its future earnings potential.

Certain suites can be tokenised at a higher price. Shopping malls and integrated projects can choose to unbundle different property rights by issuing different class of tokens, or strip the property into different income streams which are hardcoded into the ‘smart contract’.

There is no doubt that a tokenised structure can provide much flexibility for property owners or developers sitting on illiquid stocks. It can be similar or even go beyond what securitisation models or REITs (real estate investment trusts) can achieve.

However, it is important to realise that what is technically possible may not always be legally feasible. Given the dearth of regulatory guidance on IEOs at this point, there are a lot more questions than answers.

Finally, the RM100 Million Question…

In the end, literally the hundred-million-ringgit question on everyone’s minds is this: Could an IEO operator raise this kind of money, consistently? Even a mere 10% of this is a huge raise on its own, and extremely rare, by ECF standards. Where will the investors come from?

Let’s find out in Part 3.

About the Author

Edmund Yong is the managing partner of Celebrus Advisory and appointed by MDEC as part of its Talent Expert Network (formerly known as Digital Expert Panel) for blockchain technology. He is also the resident consultant for GLT Law, a multi-award-winning legal practice with specialisation in digital assets. All opinions expressed are the author’s own.

[1] Securities Commission of Malaysia, Capital Market Masterplan 3: 2021-2025 (2021).

[2] Securities Commission of Malaysia, Guideline on Digital Assets (28 October 2020).

[3] Ibid.

{kind=link}